Invest in StabilityWith Fixed Plans

Choose NCDs, Bonds & Fixed Deposits for assured income and portfolio stability.

Our Fixed Income Products

Choose from a range of fixed income instruments, carefully curated for diverse investment goals and risk appetite.

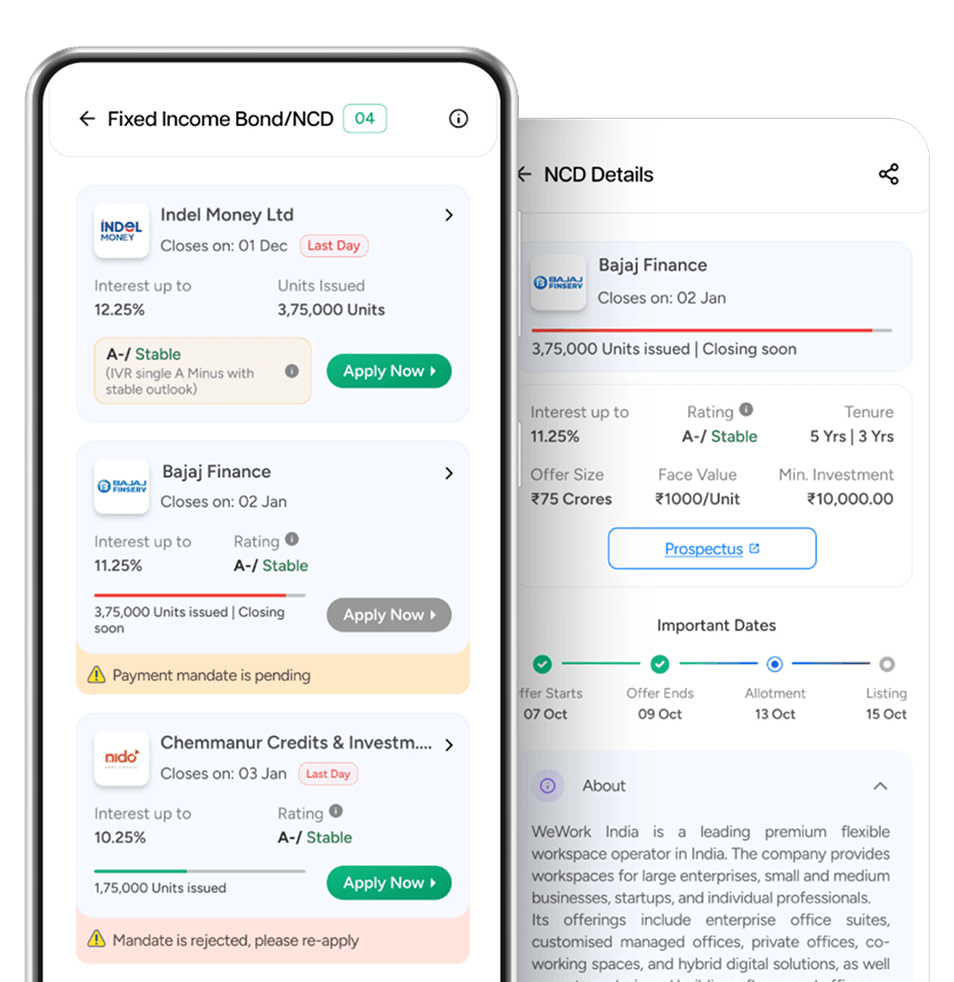

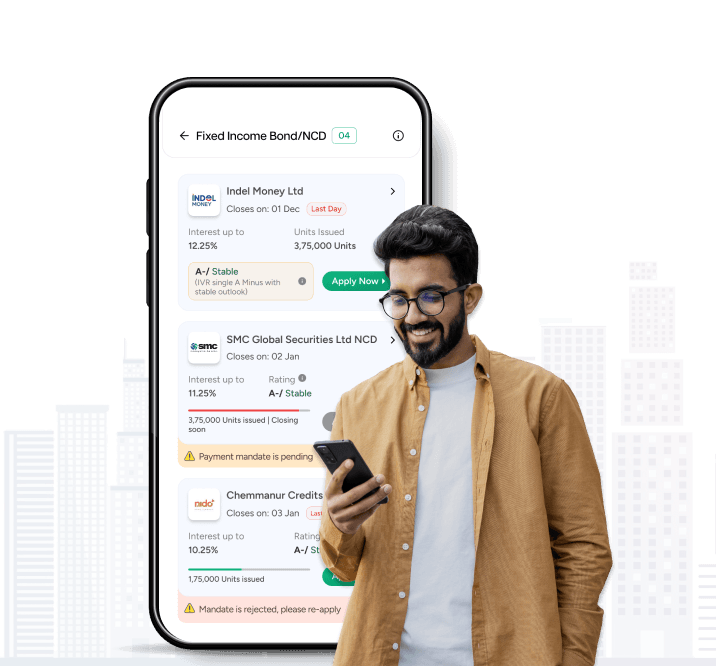

NCD

- •Higher Interest than FDs

- •Fixed Tenure Options

- •Listed on Exchange

Bonds

- •Government & Corporate Bonds

- •Regular Coupon Payments

- •Secured/Unsecured Options

Fixed Deposits

- •Bank & Corporate FDs

- •Fixed Tenure

- •Credit-Rated Instruments

RBI Floating Rate Bonds

- •Backed by Government of India

- •Ideal for Long-Term Investors

- •No Market Volatility Impact

54 EC Bonds

- •Long-Term Capital Gains Tax Exemption

- •Government-Backed Safety

- •Ideal for Tax Planning

NCD

- •Higher Interest than FDs

- •Fixed Tenure Options

- •Listed on Exchange

Bonds

- •Government & Corporate Bonds

- •Regular Coupon Payments

- •Secured/Unsecured Options

Fixed Deposits

- •Bank & Corporate FDs

- •Fixed Tenure

- •Credit-Rated Instruments

RBI Floating Rate Bonds

- •Backed by Government of India

- •Ideal for Long-Term Investors

- •No Market Volatility Impact

54 EC Bonds

- •Long-Term Capital Gains Tax Exemption

- •Government-Backed Safety

- •Ideal for Tax Planning

Why Invest with Religare Broking

Your trusted partner for fixed income investments with proven expertise and commitment to your financial success.

Regulated, Credit Rated

Access trusted, credit-rated bonds, NCDs, and fixed deposits.

Seamless Digital Process

End-to-end online investing—from discovery to execution.

Competitive & Transparent

Attractive return rates with zero hidden charges.

Personalized Support

SEBI-registered platform with dedicated relationship assistance.

How to invest in Fixed Income Products?

Start your fixed income investment journey in four simple steps

Explore Schemes

Explore curated selection of NCDs, bonds, and fixed deposits.

Compare

Analyze interest rates, credit ratings, and investment periods.

Invest Online

Complete your investment digitally with our seamless platform.

Regular Income

Receive fixed interest payments and track your portfolio growth.

Why Choose Religare Broking

We combine three decades of trust with advanced technology for seamless execution. Our clients trade with absolute confidence, backed by professional research and market insights.

30+ Years

of Trust

All-in-One,

Web and Mobile Platform

1300+

Touch Points

Client Centric

Approach

Understanding Fixed Deposit Schemes

Here is all you need to know about low cost, fixed income schemes like NCDs, Bonds and Corporate FDs.

What are Fixed Income Instruments?

Fixed-income investments offer assured returns and represent a borrowing obligation for the issuing entity. These instruments pay regular interest at a fixed rate.

The maturity value is predetermined and disclosed to investors at the time of purchase, ensuring clarity and predictability.

Due to their stable income, defined returns and lower exposure to market volatility, fixed-income investments are widely preferred by conservative investors. At Religare, our expert team carefully evaluates the risk-return profile to identify instruments that strike the right balance for your financial goals.

Especially, if you are seeking capital safety along with steady and reliable earnings over a specified period, fixed-income investments are the best option.

Supporting this, a Morgan Stanley report highlights that the fixed-income market has remained resilient amidst global uncertainty, with bonds currently offering positive after-inflation returns.

Benefits of Diversifying Your Portfolio with Fixed Income Assets

These are the key advantages of investing in fixed-income assets:

Flexible Investment Structure

Investors can choose tenures and interest payout options that suit their financial needs. Fixed deposits provide flexibility with monthly, quarterly, half-yearly or annual income options aligned to cash flow goals.

Lower Risk Profile

Fixed-income investments are less exposed to market volatility. Options with high credit ratings, such as AAA-rated deposits, offer greater safety and reliability of capital.

Stable and Predictable Income

Returns are known at the time of investment, making fixed-income options ideal for planned goals like education, retirement or major expenses, where certainty and stability are important.

Types of Fixed Income Instruments

Non-Convertible Debentures (NCDs): NCDs are debt instruments issued by companies to raise long-term capital with a fixed tenure and interest rate. They offer higher returns than traditional bank FDs and are listed on stock exchanges, providing you with the flexibility to trade them before maturity.

Corporate Bonds: Bonds are professional debt securities issued by corporations to fund business operations or expansion. They provide a reliable stream of regular coupon (interest) payments and are ideal for investors looking to diversify their portfolio with a more stable, credit-rated investment than equity.

Corporate Fixed Deposits: Corporate FDs are term deposits offered by NBFCs and companies, generally yielding higher interest rates than standard bank deposits. They are a secure way to grow your savings with guaranteed returns, making them perfect for investors with short-to-medium-term goals who seek predictability.

Trade Anytime,

Anywhere

Experience India's seamless trading app with advanced features, intuitive design, and lightning-fast execution.

Unified Portfolio

All Assets, One App

Instant Market Alerts

Live Research, Zero Delay

Seamless Security

Biometric Login for Safe Trading

Actionable Ideas

Pre-built Options Strategies

Based on 27.4K reviews

1M+

Downloads