Your ProtectionOur Responsibility

Securing your future through unbiased insurance offers, digital issuance and dedicated claims support

Quick

Policy Issuance

11+

Insurance Partners

Assisted

Claim Settlement

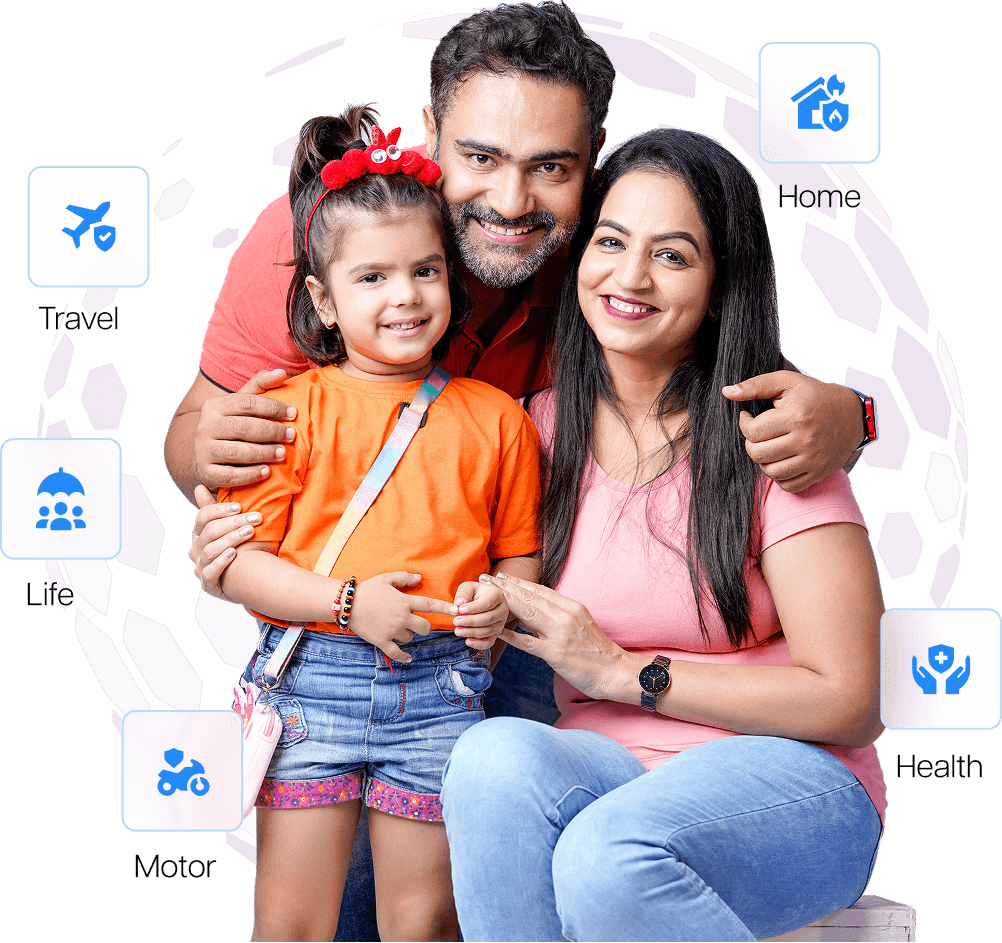

Explore Health and General Plans for All

Find the right coverage for every stage of life, all in one app.

Health Insurance

Comprehensive medical security for you and your family.

Motor Insurance

Complete protection for every journey and every vehicle.

Life Insurance

Secure your family's financial future and long-term goals.

Travel Insurance

Global coverage for medical emergencies and trip cancellations.

Home Insurance

Protect your home and belongings with complete confidence.

Business Insurance

Tailored risk protection for enterprise assets and operational continuity.

Benefits of Buying Insurance with Us

Take Home policies that protect you, your family and your future

Financial Security

Safeguard your life, health and home with reliable insurers

Peace of mind

Lead stress free life with comprehensive insurance solutions

Claims Support

Our dedicated claims support ensure hassle-free settlements

Leading Insurers

Wide choice of policies from leading insurance companies

Complete protection,

No hidden charges.

Transparent policies with trusted support.

24x7

Claims Assistance*

100%

Reliable & Secure

IRDAI

Regulated Policies**

Customer Favourites

Top-rated insurance plans chosen by thousands of customers

Care Supreme

HEALTH160+ Cashless Hospital

Entry Age (Min-Max)

Adult: 18 years onwards

Child: 91 days – 25 years

Cover Amount

₹10 lakh

Entry Age (Min-Max)

Adult: 18 years onwards

Child: 91 days – 25 years

Cover Amount

₹10 lakh

Niva Bupa Reassure 3.0

HEALTH224+ Cashless Hospital

Entry Age (Min-Max)

Adult: 18 years onwards

Child: 91 days – 30 years

Cover Amount

₹10 lakh

Entry Age (Min-Max)

Adult: 18 years onwards

Child: 91 days – 30 years

Cover Amount

₹10 lakh

ADITYA Birla ACTIV ONE MAX PLAN

HEALTH202+ Cashless Hospital

Entry Age (Min-Max)

Adult: 18 years onwards

Child: 91 days – 25 years

Cover Amount

₹10 lakh

Entry Age (Min-Max)

Adult: 18 years onwards

Child: 91 days – 25 years

Cover Amount

₹10 lakh

HDFC Ergo Optima Secure

HEALTH218+ Cashless Hospital

Entry Age (Min-Max)

Adult: 18 years onwards

Child: 91 days – 25 years

Cover Amount

₹10 lakh

Entry Age (Min-Max)

Adult: 18 years onwards

Child: 91 days – 25 years

Cover Amount

₹10 lakh

ICICI Lombard Health Elevate Plan

HEALTH137+ Cashless Hospital

Entry Age (Min-Max)

Adult: 18 years onwards

Child: 91 days – 30 years

Cover Amount

₹10 lakh

Entry Age (Min-Max)

Adult: 18 years onwards

Child: 91 days – 30 years

Cover Amount

₹10 lakh

One Platform, Multiple Partners

We have partnered with leading insurance companies. Our customers explore a wide range of policies.

Why Choose Religareonline

We provide comprehensive insurance solutions with expert guidance and competitive pricing.

30+ Years

of Trust

Best Prices

Compare quotes from top insurers to get the best deal

Quick Claims

Easy Settlement Process

Get 24/7,

Round-the-clock Support

Understanding Insurance

Here is a comprehensive guide to help you understand complex insurance jargons and understand your specific needs.

Insurance is more than just a monthly premium or a legal requirement. It is one of the important components of a financial plan. It acts as a safety net, transferring the financial risk of unforeseen events like medical emergencies, accidents, or loss of life, from your shoulders to an insurance company. By choosing the right coverage plan, you ensure that a single crisis doesn’t derail your family’s long-term financial goals.

The Pillars of Protection

In the Indian market, insurance generally falls into two categories: Life and General Insurance. Understanding the different types of insurance plans is essential for your comprehensive security.

- Life Insurance: As the name suggests, it offers financial protection against death. Term insurance and investment-linked plans (ULIPs) particularly offer high coverage and secures your family’s lifestyle and legacy. It ensures that your children’s education and your spouse’s retirement remain funded, no matter what.

- Health Insurance: With rising medical inflation, a comprehensive health plan is no longer optional. It provides access to cashless treatments at network hospitals, covering everything from hospitalization to advanced robotic surgeries and daycare procedures.

- Motor & Travel Insurance: While motor insurance is a legal mandate to protect against third-party liabilities and own-damage, travel insurance acts as a global safeguard against medical emergencies and trip cancellations during your international journeys.

Why Compare Insurance Online?

The power of a Third-Party Product (TPP) platform lies in choice. Instead of being limited to a single insurer’s catalogue, you can compare insurance quotes online from tens of leading providers. This transparency allows you to analyze:

- Claim Settlement Ratio (CSR): A critical metric of an insurer’s reliability.

- Inclusions & Exclusions: Understanding exactly what is covered under the "fine print."

- Add-on Covers: Enhancing basic policies with riders like Critical Illness or Zero Depreciation.

The Religare Edge: Beyond the Policy

As an IRDAI Registered Insurance Broker, our role doesn’t end when you buy a policy. We bridge the gap between complex insurance jargon and your specific needs. From data-backed decision making to dedicated claims advocacy, we stand beside you during the moments that matter most. We don't just sell insurance; we manage your risk lifecycle, ensuring that your protection evolves as your life does.

Trade Anytime,

Anywhere

Experience India's seamless trading app with advanced features, intuitive design, and lightning-fast execution.

Unified Portfolio

All Assets, One App

Instant Market Alerts

Live Research, Zero Delay

Seamless Security

Biometric Login for Safe Trading

Actionable Ideas

Pre-built Options Strategies

Based on 27.4K reviews

1M+

Downloads